The school plays a decisive role in stimulating aggregate demand. Aggregate demand. Keynesian AS model

According to Keynes: when aggregate effective demand falls, the government must increase its spending to stimulate production and restore full employment. The main disadvantage of the classical school is that she could not explain how to reduce unemployment, which, becoming massive, requires more and more government funds and creates an unfavorable situation.

A periodic decline in aggregate effective demand that forces government intervention may be caused by a decline in both consumer demand and investment. Keynes believed that investments are more mobile than consumption, and therefore in crises, in his opinion, Insufficient aggregate investment demand was to blame.

Keynesian theory views monetary policy primarily from the point of view of its influence on overall spending, effective demand and employment, from this point of view it directs attention to relationship between interest rate and investment.

Central banks have at their disposal three tools through which they can influence the quantity of money and the terms of credit: the discount rate, control of bank reserves and so-called free market operations. By changing the required reserve ratio, the central bank influences mainly bank deposits in current accounts; commercial banks, however, have various opportunities to avoid this. Therefore, from the late 30s, especially in connection with the expansion of attempts to regulate monetary circulation, operations began to be carried out on the free market, which assumed wide demand for government securities. If the central bank buys government bonds and thereby increases their value, it increases liquidity, and conversely, if it sells government bonds, then it reduces the amount of cash in circulation. Given the colossal public debt that is now typical of all countries, free market operations become a manifestation of concern for the stability of the government securities market.

Let us recall the Keynesian ideas about the influence of monetary policy on effective demand. If the amount of money increases, this makes it possible to more fully satisfy the need for liquid reserves. Finally, some of them become redundant, the propensity for liquidity and the interest rate decrease. Excess savings are used partly to purchase consumer goods and thereby increase consumer demand, and partly to purchase securities, which again expands investment demand. An increase in income means an increase in savings, but even more so in investments, because the interest rate has fallen.

True, monetary policy would become completely ineffective if the economy reached the so-called liquidity belts. In this hypothetical situation, the "level of confidence" is so low that the entire influx of additional money disappears into cash reserves, and even the lowest rate of interest is unable to revive investment activity. The demand for money is almost endless. This case has a “rational” grain, at least in the fact that even the most favorable general interest conditions will not yield anything if the general state of affairs and the resulting possibilities of debtors do not provide real grounds for credit.

Monetary policy should, therefore, influence economic activity primarily through its impact on the interest rate, since the volume of investment depends on it. But the experience of recent decades shows that the effectiveness of monetary policy is very limited. Keynes himself openly admitted this: “The state will have to exercise its guiding influence on the propensity to consume partly through an appropriate system of taxes, partly by fixing the rate of interest and partly, perhaps, in other ways. Moreover, it seems unlikely that the effect of banking policy on the rate of interest would by itself be sufficient to ensure the optimal amount of investment. I imagine, therefore, that a sufficiently broad socialization of investment will be the only means to ensure an approach to full employment...”

After the Second World War, the main instrument of state-monopoly regulation became financial policy, based on the use of the state budget. Its main task is to control aggregate demand on the basis of macroeconomic relationships discovered by Keynesian analysis, and to fill the gaps caused by excess savings, in this case insufficient investment in the private sector of the economy. This change is designated as a transition to “active” government policy; this means that the role of the state budget is no longer limited to covering the inevitable expenses of the state. The budget must influence the entire social process of reproduction and thereby ensure the general conditions for the functioning of the economic system. The state budget acts as the most vivid embodiment of all processes of socialization that take place in the modern world and make centralized regulation necessary, which in these conditions can only be carried out through the state budget.

Issues for discussion

What is the revolutionary nature of Keynes's theory? What do you think are the reasons for the emergence of Keynesian theory during the historical period in question? Why is Keynes's theory called the theory of aggregate demand? Why did Keynes criticize Say's law? Why, according to Keynesian theory, is government intervention in the economy necessary? According to Keynes, the cause of macro-disequilibrium in the economy is the mismatch between savings and investments? Do you agree with this statement? According to Keynesian theory, aggregate demand lags behind income - why? Do you agree with Keynes's arguments? What specific tools did Keynes propose to stimulate aggregate demand? What specific tools did Keynes propose to stimulate investment? What is a multiplier? How does it work? Give an example. What reasons can slow down the action of the multiplier? What is the main disadvantage of the classical school? What did Keynes propose in this regard? Do you agree with his views on this problem? Do you agree with Keynes's opinion that the main cause of economic crises is insufficient investment demand? As you know, Keynes considered monetary policy only in the context of regulating effective demand. According to Keynes, how does monetary policy affect effective demand? What does the Keynesian liquidity belt mean? What are the functions of the state in the economy according to the Keynesian concept?

Guidelines. Preparation for seminar classes should begin by studying the lecture notes and recommended literature. When studying this topic, pay special attention to consideration of equilibrium issues in the AD-AS model and macroeconomic stabilization policy. It is advisable to conduct one of the SRSP classroom sessions in the form of a case discussion.

Fiscal policy is used to influence both aggregate demand and aggregate supply.

Stimulating Aggregate Demand

If the government increases payments to households (social assistance) or reduces their taxation, households increase their consumption and demand (demand-side policy). It has been empirically established that households that have a modest list of consumed goods and services usually, when their income increases, allocate almost all their money to consumption and save only a small part of the money (we are talking about a strong propensity to consume). But in order to accelerate economic growth, it is not enough to simply “distribute purchasing power.” In practice, depending on the specific situation, certain restrictions and contradictions arise: households can begin to save all or almost all their free money without increasing consumption. People take into account the interests of the future in their actions - changes in their consumption may not depend on changes in current income. people can increase their consumption of imported goods (if domestic production capacity does not match the new demand structure) and actually sponsor the economy of the importing country. In this case, economic growth occurs abroad, and not within the country, etc.

To eliminate such situations, the state is often forced to increase the tax burden.

Stimulating Aggregate Supply

If the state reduces taxes on enterprises and increases the amount of its assistance to them, the competitiveness of the national economy - all other things being equal - will increase. The costs of commodity producers will decrease, as a result of which prices for their products will decrease, purchasing power will indirectly increase, people will begin to buy more goods and services, this will lead to increased productivity, an influx of investment, an increase in the supply of jobs and a reduction in unemployment. Increasing the profits of enterprises will allow them to increase investment, which will lead to GDP growth. But such a scenario may not come true, for example, if: enterprises do not invest additional profits, but distribute them among shareholders. It's even worse if the shareholders are foreigners. Then, as in the situation with demand-side policies, economic growth occurs outside the country. In order for enterprises to invest, it is necessary to create favorable legislative conditions.

Displacement effect

If the government borrows money to finance economic growth (both in conditions of stimulating demand and in conditions of stimulating supply), it needs to offer conditions that are more favorable than those for other borrowers, enterprises and households. It becomes more difficult for the latter to borrow, interest rates rise, the number of consumer loans falls, investment declines, all this counteracts economic growth.

In the event of a strong deterioration in economic conditions, the government can implement a fiscal policy based on maintaining short-term economic activity, bringing into play the “Keynesian multiplier.” The Keynesian multiplier is a macroeconomic mechanism identified by Keynes, which makes it possible to compensate for the insufficiency of private spending with government spending. Indeed, an increase in government spending generates additional income, which is partly spent on consumption, partly on savings, and partly returned to government agencies in the form of taxes and insurance premiums. Part of the additional income allocated for consumption accounts for the increase in domestic consumption of goods and services of enterprises. The latter can then increase investment and the number of jobs and distribute additional income. Therefore, an increase in government spending has a cumulative effect (multiplier effect) that stimulates economic activity.

Governments can also support economic activity by cutting personal taxes, but this measure stimulates economic growth to a lesser extent than a policy of increasing government spending. After all, the additional income received in the form of tax exemption is immediately saved by households or businesses.

REVIEW QUESTIONS What are the functions of the state budget? What are automatic stabilizers? List the instruments of stimulating fiscal policy. List the instruments of contractionary fiscal policy. How can the government stimulate demand within the framework of fiscal policy? How can the government stimulate supply as part of fiscal policy? What is the “crowding out effect”?

More on the topic STIMULATING AGGREGATE DEMAND AND AGGREGATE SUPPLY:

- Chapter 9 GENERAL MACROECONOMIC EQUILIBRIUM: MODEL OF AGGREGATE DEMAND AND AGGREGATE SUPPLY

- Chapter 3 Definition of Output: Introduction of Aggregate Supply and Aggregate Demand

- CHAPTER 4. GENERAL MACROECONOMIC EQUILIBRIUM: AGGREGATE DEMAND AND AGGREGATE SUPPLY

- Chapter 4. Aggregate demand, aggregate supply and macroeconomic equilibrium

The totality of final goods) that consumers, businesses and the government are willing to buy (for which there is demand in the country's markets) at a given price level (at a given time, under given conditions).

Aggregate demand () is the sum of planned expenses for the purchase of final products; it is the real output that consumers (including firms and governments) are willing to buy at a given price level. The main factor influencing this is the general price level. Their relationship is reflected by the curve, which shows the change in the total level of all expenses in the economy depending on changes in the price level. The relationship between real output and the general price level is negative or inverse. Why? To answer this question, it is necessary to identify the main components: consumer demand, investment demand, government demand and net exports, and analyze the impact of price changes on these components.

Aggregate demand

Consumption: As the price level rises, real purchasing power falls, causing consumers to feel less wealthy and therefore buy a smaller share of real output than they would have bought at the same price level.

Investments: An increase in the price level usually leads to an increase in interest rates. Credit becomes more expensive, which deters firms from making new investments, i.e. an increase in the price level, affecting interest rates, leads to a decrease in the second component - the real volume of investment.

Government procurement of goods and services: to the extent that state budget expenditure items are determined in nominal monetary terms, the real value of government purchases will also decrease as the price level rises.

Net exports: As the price level in one country rises, imports from other countries will rise and exports from that country will fall, resulting in a fall in real net exports.

Equilibrium price level and equilibrium output

Aggregate supply and demand influence the establishment of the equilibrium general price level and the equilibrium volume of production in the economy as a whole.

All other things being equal, the lower the price level, the larger part of the national product consumers will want to purchase.

The relationship between the price level and the real volume of the national product that is in demand is expressed by the aggregate demand schedule, which has a negative slope.

The dynamics of consumption of the national product are influenced by price and non-price factors. The effect of price factors is realized through a change in the volume of goods and services and is expressed graphically by movement along a curve from point to point. Non-price factors cause a change in , shifting the curve left or right to or .

Price factors other than price level:

Non-price determinants (factors) influencing aggregate demand:

- Consumer spending, which depends on:

- Consumer welfare. As wealth increases, consumer spending increases, that is, AD increases

- Consumer expectations. If an increase in real income is expected, then expenses in the current period increase, that is, AD increases

- Consumer debts. Debt reduces current consumption and AD

- Taxes. High taxes reduce aggregate demand.

- Investment costs, which include:

- Changes in interest rates. An increase in the interest rate will lead to a decrease in investment spending and, accordingly, a decrease in aggregate demand.

- Expected returns on investment. With a favorable prognosis, AD increases.

- Business taxes. When taxes increase, AD decreases.

- New technologies. Usually lead to an increase in investment spending and an increase in aggregate demand.

- Excess capacity. They are not fully used, there is no incentive to build up additional capacity, investment costs are reduced and AD falls.

- Government spending

- Net Export Expenses

- National income of other countries. If the national income of countries increases, then they increase purchases abroad and thereby contribute to an increase in aggregate demand in another country.

- Exchange rates. If the exchange rate for its own currency increases, then the country can purchase more foreign goods, and this leads to an increase in AD.

Aggregate offer

Aggregate supply is the real volume that can be produced at different (certain) price levels.

The law of aggregate supply - at a higher price level, producers have incentives to increase production volume and, accordingly, the supply of manufactured goods increases.

The aggregate supply graph has a positive slope and consists of three parts:

- Horizontal.

- Intermediate (ascending).

- Vertical.

Non-price factors of aggregate supply:

- Changes in resource prices:

- Availability of internal resources

- Prices for imported resources

- Market dominance

- Change in productivity (production volume/total costs)

- Legal changes:

- Business taxes and subsidies

- Government regulation

Aggregate supply: classical and Keynesian models

Aggregate offer() is the total amount of final goods and services produced in the economy; it is the total real output that can be produced in a country at various possible price levels.

The main factor influencing , is also the price level, and the relationship between these indicators is direct. Non-price factors are changes in technology, resource prices, taxation of firms, etc., which is graphically reflected by a shift of the AS curve to the right or left.

The AS curve reflects changes in total real output as a function of changes in the price level. The shape of this curve largely depends on the time period in which the AS curve is located.

The difference between the short and long term in macroeconomics is associated mainly with the behavior of nominal and real quantities. In the short term, nominal values (prices, nominal wages, nominal interest rates) change slowly under the influence of market fluctuations and are “rigid”. Real values (output volume, employment level, real interest rate) change significantly and are considered “flexible”. IN long term the situation is exactly the opposite.

Classic AS model

Classic AS model describes the behavior of the economy in the long run.

In this case, the AS analysis is built taking into account the following conditions:

- the volume of output depends only on the number of production factors and technology;

- changes in factors of production and technology occur slowly;

- the economy operates at full employment and output is equal to potential;

- prices and nominal wages are flexible.

Under these conditions, the AS curve is vertical at the level of output at full employment of production factors (Fig. 2.1).

Shifts in AS in the classical model are possible only when the value of production factors or technology changes. If there are no such changes, then the AS curve in the short run is fixed at the potential level, and any changes in AD are reflected only in the price level.

Classic AS model

- AD 1 and AD 2 - aggregate demand curves

- AS - aggregate supply curve

- Q* is the potential production volume.

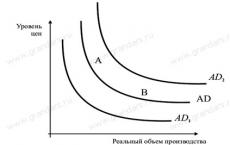

Keynesian AS model

Keynesian AS model examines the functioning of the economy in the short term.

The analysis of AS in this model is based on the following premises:

- the economy operates under conditions of underemployment;

- prices and nominal wages are relatively rigid;

- real values are relatively mobile and quickly respond to market fluctuations.

The AS curve in the Keynesian model is horizontal or has a positive slope. It should be noted that in the Keynesian model the AS curve is limited on the right by the level of potential output, after which it takes the form of a vertical straight line, i.e. actually coincides with the long-term AS curve.

Thus, the volume of AS in the short term depends mainly on the value of AD. In conditions of underemployment and price rigidity, fluctuations in AD primarily cause a change in output (Figure 2.2) and only subsequently can be reflected in the price level.

Keynesian AS model

So, we looked at two theoretical models of AS. They describe different reproduction situations that are quite possible in reality, and if we combine the assumed forms of the AS curve into one, we will get an AS curve that includes three segments: horizontal, or Keynesian, vertical, or classical, and intermediate, or ascending.

Horizontal segment of the AS curve consistent with a recessionary economy, high unemployment and underutilized production capacity. Under these conditions, any increase in AD is desirable, since it leads to an increase in output and employment without increasing the general price level.

Intermediate segment of the AS curve assumes a reproduction situation where an increase in real production volume is accompanied by a slight increase in prices, which is associated with the uneven development of industries and the use of less productive resources, since more efficient resources are already used.

Vertical segment of the AS curve occurs when the economy is operating at full capacity and it is no longer possible to achieve further growth in output in the short term. An increase in aggregate demand under these conditions will lead to an increase in the general price level.

General AS model.

- I - Keynesian segment; II - classic segment; III - intermediate segment.

Macroeconomic equilibrium in the AD-AS model. Ratchet effect

The intersection of the AD and AS curves determines the macroeconomic equilibrium point, the equilibrium output volume and the equilibrium price level. A change in equilibrium occurs under the influence of shifts in the AD curve, the AS curve, or both.

The consequences of an increase in AD depend on which segment of AS it occurs on:

- on the horizontal segment AS, an increase in AD leads to an increase in real output at constant prices;

- on the vertical segment AS, an increase in AD leads to an increase in prices with a constant volume of output;

- in the intermediate segment AS, an increase in AD generates both an increase in real output and a certain increase in prices.

Reducing AD should lead to the following consequences:

- on the Keynesian segment AS, real output will decrease and the price level will remain unchanged;

- in the classic segment, prices will fall, and real output will remain at full employment;

- In the intermediate period, the model assumes that both real output and the price level will decline.

However, there is one important factor that modifies the effects of AD reduction in the classic and intermediate periods. The reverse movement of AD from position in (Fig. 2.4) may not restore the original equilibrium, at least in the short term. This is due to the fact that prices for goods and resources in the modern economy are largely inflexible in the short term and do not show a downward trend. This phenomenon is called the ratchet effect (a ratchet is a mechanism that allows the wheel to turn forward, but not backward). Let us consider the effect of this effect using Fig. 2.4.

Ratchet effect

The initial growth of AD, to the state, led to the establishment of a new macroeconomic equilibrium at the point, which is characterized by a new equilibrium price level and production volume. A fall in aggregate demand from the state to will not lead to a return to the initial equilibrium point, since increased prices do not tend to decrease in the short term and will remain at the level. In this case, the new equilibrium point will move to the state, and the real level of production will decrease to the level.

As we found out, the ratchet effect is associated with price inflexibility in the short term.

Why do prices not tend to decrease?

- This is primarily due to the inelasticity of wages, which accounts for approximately ¾ of the firm's expenses and significantly affects the price of products.

- Many firms have significant monopoly power to resist lower prices during periods of falling demand.

- Prices for some types of resources (other than labor) are fixed by the terms of long-term contracts.

However, in the long run, when prices fall, prices will go down, but even in this case, the economy is unlikely to be able to return to its original equilibrium point.

Rice. 1. Consequences of AS growth

AS Curve Offset. As aggregate supply increases, the economy moves to a new equilibrium point, which will be characterized by a decrease in the general price level while a simultaneous increase in real output. A decrease in aggregate supply will lead to higher prices and a decrease in real NNP

(Fig. 1 and 2).

So, we examined the most important macroeconomic indicators - aggregate demand and aggregate supply, identified the factors influencing their dynamics, and analyzed the first model of macroeconomic equilibrium. This analysis will serve as a springboard for a more detailed study of macroeconomic issues.

Rice. 2. Consequences of the fall of AS

Keynesian model for determining equilibrium output, income and employment

To determine the equilibrium level of national production, income and employment, the Keynesian model uses two closely interrelated methods: the method of comparing aggregate expenditures and output and the method of “withdrawals and injections”. Let's consider the first method "expenses - production volume". To analyze it, the following simplifications are usually introduced:

- there is no government intervention in the economy;

- the economy is closed;

- the price level is stable;

- there is no retained earnings.

Under these conditions, total spending is equal to the sum of consumption and investment spending.

To determine the equilibrium volume of national production, the investment function is added to the consumption function. The total expenditure curve intersects the line at an angle of 45° at the point that determines the equilibrium level of income and employment (Fig. 3).

This intersection is the only point at which total costs are equal. No level of NNP above the equilibrium level is sustainable. Inventories of unsold goods rise to undesirable levels. This will encourage entrepreneurs to adjust their activities in the direction of reducing production volume to the equilibrium level.

Rice. 3. Determination of equilibrium NNP using the "expenses - production volume" method

At all potential levels below the equilibrium, the economy tends to spend more than entrepreneurs produce. This encourages entrepreneurs to expand production to the equilibrium level.

Extraction and injection method

The method of determining by comparing expenditures and output makes it possible to clearly present total expenditures as a direct factor determining levels of production, employment and income. Although the cap-and-inject method is less straightforward, it has the advantage of focusing on inequality and NNP at all but equilibrium levels of output.

The essence of the method is as follows: given our assumptions, we know that the production of any volume of output will provide an adequate amount of income after taxes. But it is also known that households can save part of this income, i.e. do not consume. Saving, therefore, represents the withdrawal, leakage, or diversion of potential expenditure from the expenditure-income stream. As a result of saving, consumption becomes less than total output, or NNP. In this regard, consumption by itself is not enough to remove the entire volume of production from the market, and this circumstance, apparently, leads to a decrease in total production. However, the business sector does not intend to sell all products only to final consumers. Some of the production takes the form of means of production, or investment goods, which will be sold within the business sector itself. Therefore, investment can be viewed as an injection of expenditure into the income-expenditure flow, which complements consumption; in short, investments represent potential compensation, or reimbursement, for withdrawals from savings.

If the withdrawal of funds from savings exceeds the injection of investment, then the NNP will be less, and the given level of NNP will be too high to be sustainable. In other words, any level of NNP where saving exceeds investment will be above the equilibrium level. Conversely, if the injection of investment exceeds the leakage of funds to savings, then there will be more than the NNP, and the latter should rise. Let us repeat: any amount of NNP when investment exceeds saving will be below the equilibrium level. Then, when, i.e. When the leakage of funds to savings is fully compensated by injections of investment, total spending equals output. And we know that such equality determines the equilibrium of the NPP.

This method can be illustrated graphically using saving and investment curves (Figure 3.6). The equilibrium volume of NNP is determined by the point of intersection of the saving and investment curves. Only at this point the population intends to save as much as entrepreneurs want to invest, and the economy will be in a state of equilibrium.

Change in equilibrium NNP and multiplier

In the real economy, NNP, income and employment are rarely in a state of stable equilibrium, but are characterized by periods of growth and cyclical fluctuations. The main factor influencing the dynamics of NNP is fluctuations in investment. In this case, a change in investment affects the change in NNP in a multiplied proportion. This result is called the multiplier effect.

Multiplier = Change in real NNP / Initial change in expenditure

Or, rearranging the equation, we can say that:

Change in NNP = Multiplier * Initial change in investment.

Three points should be made from the outset:

- The "initial change in spending" is usually caused by shifts in investment spending for the simple reason that investment appears to be the most volatile component of total spending. But it should be emphasized that changes in consumption, government purchases or exports are also subject to the multiplier effect.

- An "initial change in expenditure" means a movement up or down in the total expenditure schedule due to a downward or upward shift in one of the components of the schedule.

- From the second remark it follows that the multiplier is a double-edged sword that acts in both directions, i.e. a slight increase in spending can result in a multiple increase in NNP; on the other hand, a small reduction in spending can lead through the multiplier to a significant decrease in NNP.

To determine the value of the multiplier, the marginal propensity to save and the marginal propensity to consume are used.

Multiplier = or =

The meaning of the multiplier is as follows. A relatively small change in the investment plans of entrepreneurs or the saving plans of households can cause much larger changes in the equilibrium level of NNP. The multiplier amplifies fluctuations in business activity caused by changes in spending.

Note that the larger (less) the multiplier will be. For example, if - 3/4 and, accordingly, the multiplier - 4, then a decrease in planned investments in the amount of 10 billion rubles. will entail a decrease in the equilibrium level of NNP by 40 billion rubles. But if it is only 2/3, and the multiplier is 3, then the reduction in investment is the same 10 billion rubles. will lead to a drop in NNP by only 30 billion rubles.

The multiplier as presented here is also called the simple multiplier for the sole reason that it is based on a very simple economic model. Expressed as 1/MPS, the simple multiplier reflects only savings withdrawals. As stated above, in reality, the sequence of income and expenditure cycles may be attenuated due to withdrawals in the form of taxes and imports, i.e. In addition to the leakage to savings, one part of the income in each cycle will be withdrawn in the form of additional taxes, and the other part will be used to purchase additional goods abroad. Taking these additional exceptions into account, the formula for the 1/MPS multiplier can be modified by substituting one of the following indicators instead of MPS in the denominator: “the share of changes in income that is not spent on domestic production” or “the share of changes in income that “leaks” or is withdrawn from the income-expenditure flow. A more realistic multiplier, which is obtained taking into account all these withdrawals - savings, taxes and imports, is called a complex multiplier.

Equilibrium output in an open economy

So far, in the aggregate expenditure model we have abstracted from foreign trade and assumed the existence of a closed economy. Let us now remove this assumption, take into account the presence of exports and imports, and the fact that net exports (exports minus imports) can be either positive or negative.

What is the ratio of net exports, i.e. exports minus imports, and total expenditures?

First of all, let's look at exports. Like consumption, investment and government purchases, exports cause growth in domestic output, income and employment. Although goods and services that cost money to produce go overseas, spending by other countries on American goods leads to expanded production, more jobs, and higher incomes. Therefore, exports should be added as a new component to total expenditure. Conversely, when an economy is open to international trade, we must recognize that part of the expenditure earmarked for consumption and investment will go to imports, i.e. for goods and services produced abroad rather than in the United States. Consequently, in order not to inflate the cost of domestic production, the amount of expenditure on consumption and investment must be reduced by the part that goes to imported goods. Thus, when measuring total expenditures on domestically produced goods and services, import expenditures must be subtracted. In short, for a private, non-trading, or closed, economy, total expenditure is , and for a trading, or open, economy, total expenditure is . Recalling that net exports are , we can say that total spending for a private, open economy is

.

3.7. The impact of net exports on NMP

From the very definition of net exports it follows that they can be either positive or negative. Therefore, exports and imports cannot have a neutral effect on equilibrium NNP. What is the real impact of net exports on NNP?

Positive net exports leads to an increase in total expenditures compared to their value in a closed economy and, accordingly, causes an increase in the equilibrium NMP (Fig. 3.7). On the graph, the new point of macroeconomic equilibrium will correspond to the point, which is characterized by an increase in real NNP.

Negative net exports on the contrary, it reduces domestic aggregate expenditure and leads to a decrease in domestic NNP. On the graph there is a new equilibrium point and the corresponding volume of NNP - .

Evolution of theoretical views on the role

REGULATION OF THE NATIONAL ECONOMY.

Economists at different times conceptualized and understood methodological approaches to the implementation of macroeconomic equilibrium in different ways. In scientific views on this problem, several stages in the development of the theory of economic equilibrium and corresponding practical options for solving this problem can be distinguished. The criterion for identifying these stages is the degree of external restriction of the freedom of choice of an economic entity. And since the external limiter, as a rule, is the state, the criterion for identifying the stages of economic theory can be defined as the degree of government intervention in the process of establishing the economic equilibrium of the national economy.

Classical theory. The first stage is the so-called “classical theory” of economic equilibrium, the largest representatives of which are A. Smith and J. Say. According to A. Smith, in the conditions of division of labor, each person, guided by selfish motives and pursuing only his own interest, thereby satisfies the interests of society (“the invisible hand of the market”) and increases the “wealth of the nation.” On the basis of "natural harmony" Smith develops the idea of natural balance. In his opinion, it is established spontaneously in the economy in the absence of external (state) intervention and is the optimal mode of functioning of the economic system.

Say J.B. formulated the law of the market, according to which the exchange of labor products automatically leads to equilibrium between purchase and sale. Supply creates its own demand. The income received from the production of any total volume of output, once spent, must be sufficient to meet the total demand. If demand lags behind supply, it is necessary to reduce the level of wages and, due to this, reduce prices for the goods offered. A general decrease in demand for goods will be reflected in a decrease in demand for labor and other resources. The demand for labor is slowly falling. Competition among the unemployed will make wage rates so low that it will be profitable for entrepreneurs to hire everyone who wants to work. Involuntary unemployment is impossible. Anyone willing to work at a market-determined wage rate can easily find a job. Competition in the labor market eliminates involuntary unemployment.

All this taken together characterizes the elasticity of the price-wage ratio. Thus, fluctuations in the interest rate and the elasticity of the price-wage ratio act as market regulation levers that are quite capable of maintaining full employment and, thereby, creating sufficient conditions for general economic equilibrium. The economy as a whole is turning into a self-regulating mechanism, for which government intervention is not only unnecessary, but even harmful.

The fiasco of free Classical equilibrium theory

market. was quite sufficient for a certain level of economic development. When economic conditions changed qualitatively, this theory turned out to be insufficient. Failures (fiascos) of automatic self-regulation of a free and spontaneous market economy emerged. The technological revolution of the late nineteenth century gave rise to numerous and varied changes in the economy. The growth of productive forces and labor productivity gave rise to a qualitative leap in the quantity and range of goods produced. Monopolization of the economy has practically destroyed free competition and thereby undermined the basis for free fluctuations in prices and wages. Monopolization pushed aside individual supply and individual demand and replaced it with a much more aggregated supply and demand. With the development of monopolism, a gap between aggregate supply and aggregate demand began to accumulate. Quantitative discrepancies, having reached a certain level, turned into an economic crisis of overproduction.

The operating conditions of the economic system changed, and these changes turned out to be so significant that aggregate demand began to lag behind aggregate supply at an increasing, accelerated pace. All this was expressed in the catastrophic crisis of overproduction of 1929-1933, where it was the economic catastrophe that put forward the social order for a new economic theory of macroequilibrium, the specific exponent of which was D. Keynes.

Economic In the emergence of a new theory of macro -

views economic equilibrium D. Keynes

D. Keynes. played such an important role that his name turned out to be inextricably linked with the “new economic theory of aggregate demand.” Keynes proved that all the stabilizing forces that had previously been steadily operating were no longer sufficient in a rich, industrialized country. The starting points of Keynesian theory are as follows:

Firstly, demand increases more slowly than supply, as more and more of the income goes into savings. As a result, the macroeconomic balance is disrupted and cannot be restored automatically. Secondly, certain, even small changes in demand can cause significant changes in production and employment, since the feedback mechanism repeatedly increases the supply of goods. Third, the relationship between income, investment, savings and expectations creates an uncontrollable and unpredictable final result with the inaction of automatic regulators at the macroeconomic level.

The general conclusion: if entrepreneurs do not want to invest as much as is needed for full employment, the state should do it. Therefore, programs of “compensatory” expansion of demand on the part of the state are being put forward at the center of economic impact. The most effective means is to increase government spending, which triggers the multiplier mechanism.

The main idea of D. Keynes is that in conditions of lagging demand, it is necessary to propose and implement measures to activate and stimulate aggregate demand. This should cause an expansion of production and a decrease in unemployment.

Keynes's theory is the theory of "effective demand". Effective demand is the aggregate effective demand that determines and ensures the volume of employment. Keynes's idea: it is necessary to stimulate demand through government intervention in the reproduction process. Government stimulation of aggregate demand is called “expansion policy.” This policy has a special property called the “multiplier effect.” Cartoonist– increase, multiplication, multiple increase. Multiplier effect is that the total increase in national income ultimately exceeds government spending on stimulating aggregate demand. In addition to the primary effect, secondary, tertiary, etc. occur. effects. Employment in one industry generates employment in several others related to the first industry. The concept of a multiplier can be expressed by the formula:

where M is the multiplier, ND is national income, I is investment or government spending to stimulate demand.

Keynes proposed two ways to stimulate demand: a) monetary policy is a reduction in the interest rate for loans; b) fiscal policy - providing tax benefits and subsidies, as well as increasing government spending to increase incomes for the poor. All these measures cause productivity growth, employment growth, and demand growth. But this is also a path to inflation. However, Keynes believed that inflation could be controlled.

Keynes argued that it was possible, with the help of public investment, as well as credit and monetary policy, to introduce some planned principles into a macroeconomy that had lost the ability to self-regulate.

The Keynesian theory of aggregate demand determined a qualitatively new moment in the development of the economic system. It is with the application of Keynes' theory that the national economy turns into an integral organic system, which can justifiably be called macroeconomics in contrast to microeconomics. Within the framework of this theory, an economic mechanism was formed to contain market forces by covering the entire macroeconomy with state regulation. Based on Keynes's theory, a long-term trend towards increasing the influence of the state on the macroeconomic equilibrium has formed and continues to develop.

In The General Theory of Employment, Interest and Money, John Maynard Keynes (1883–1946) focused on the inefficiency of consumer demand. It is demand, in his opinion, that plays a decisive role in stimulating and developing production.

Aggregate demand is the sum of consumer spending and investment.

If aggregate demand is greater than supply, then production growth incentives work. In this case, aggregate demand is truly effective and contributes to high employment and fuller use of production capacity.

The main components of aggregate demand are consumption, investment and government spending. The main factors influencing aggregate demand: propensity to consume, expected return on investment, liquidity preference.

In Keynes's theory, national income Y and the level of employment N are dependent variables. The size of national income determines the level of employment. National income itself, on the one hand, acts as a factor influencing the growth of consumer demand (consumer demand grows, but not to the same extent as income); on the other hand, the growth of national income depends on investment.

Consumption expenditures are determined by the propensity to consume C/C. There is a psychological law at work here that expresses the relationship between consumption and income. As income increases, the average propensity to consume falls under the influence of a decrease in the marginal propensity to consume (ΔС/ΔY).

The level of investment demand / depends on the expected efficiency of capital p" and the interest rate r. The interest rate, or interest rate, is the payment for parting with liquidity. Liquidity preference is the desire to own money, to preserve savings in cash form.

Percent r is a function of the demand for money (liquidity preference) and the amount of money in circulation (money supply).

Keynes's theory is called the theory of effective demand, thereby highlighting the main idea. And it consists in activating and stimulating aggregate demand (general purchasing power) to influence the production and supply of goods and services and increase the level of employment.

The significance of J.M. Keynes's theory lies not simply in the revision of traditional approaches to the analysis of economic development processes. Keynes laid the general theoretical foundations for the study of functional dependencies and interrelations of real economic quantities as aggregated categories, and showed their influence on the course and trends of economic development.

The Keynesian revolution involves the use of an active economic policy, taking into account social, psychological, and organizational factors.

Modern economic theory is in one way or another connected with the theory and methodology of Keynes. It cannot ignore the broad interpretation of the subject of economic science, the influence of diverse conditions and factors on the processes of economic development.

63.Modern Western economic schools (F. Hayek, V. Eucken, L. Erhard, M. Friedman).

The emergence of liberalism as a current of Western economic thought dates back to the 18th century. It is based on the political philosophy of liberalism, the credo of which - the famous principle of “laisser faire” (“do not interfere with action”) - can be revealed as allowing people to do what they want, giving them the right to be themselves in economic activity and in religion, culture, everyday life and thought.

Neoliberalism- a direction in economic science and the practice of economic activity, based on the principle of self-regulation of the economy, free from excessive regulation.

Modern representatives of economic liberalism follow two, to a certain extent traditional, positions: firstly, they proceed from the fact that the market (as the most effective form of economic management) creates the best conditions for economic growth, and, secondly, they defend the priority importance of freedom participants in economic activity. The state must provide conditions for competition and exercise control where these conditions do not exist. In practice (and this is what neoliberals are forced to admit in most cases), the state now intervenes in economic life on a wide scale and in various forms.

In fact, under the name of neoliberals there is not one, but several schools.

The Chicago (M. Friedman), London (F. Hayek), and Freiburg (W. Eucken, L. Erhard) schools are usually classified as neoliberalism.

Modern liberals are united by a common methodology, and not conceptual provisions. Some of them adhere to the right (opponents of the state, preachers of absolute freedom), others - to the left (a more flexible and sober approach to the participation of the state in economic activity) views. Supporters of neoliberalism usually criticize Keynesian methods of regulating the economy. In the United States and some other Western countries, modern neoliberal policies are based on a number of economic approaches that have received the most recognition. This is monetarism, which assumes that the capitalist economy has internal regulators and management should rely primarily on monetary instruments; supply-side economics, which emphasizes economic incentives; theory of rational expectations: the availability of information allows one to foresee the consequences of economic decisions.

In general, the strengthening of the ideas of liberalism was greatly facilitated by the success of economic policies based on the principles of economic freedom, which were carried out by the governments of leading Western countries at different periods. The most indicative in this regard is the experience of Germany, Great Britain and the USA. The International Monetary Fund also largely builds its activities based on the ideas of liberalism, in particular monetarism.